Protecting Retirement Income from Sequence Risk

Investment RetirementPlanning for retirement involves many moving parts saving diligently, investing wisely, and aligning your strategy with long-term goals. While you can control many of these decisions, one critical factor remains unpredictable: sequence risk.

Sequence risk refers to the possibility of experiencing poor investment returns early in retirement. While market volatility is a normal part of investing, the order in which returns occur can significantly impact how long your portfolio lasts. Two retirees can earn the exact same average return over time yet end up with dramatically different outcomes depending on when gains and losses occur. Because no one can predict the sequence they’ll experience, it’s important to plan for a range of possible outcomes.

Why Sequence Risk Matters

It’s no secret that global stock markets are volatile. During your working years, market volatility can work in your favor. As you consistently contribute to your investments, downturns allow you to buy more shares at lower prices, potentially strengthening long-term growth.

In retirement, however, the situation reverses. Instead of contributing to your portfolio, you begin withdrawing from it. If markets decline early in retirement, you may be forced to sell investments at lower prices to fund your expenses. This reduces the number of shares remaining in your portfolio, limiting its ability to recover when markets rebound. This is the essence of sequence risk: early losses can have a lasting negative impact, even if long-term returns are strong.

A Simple Illustration

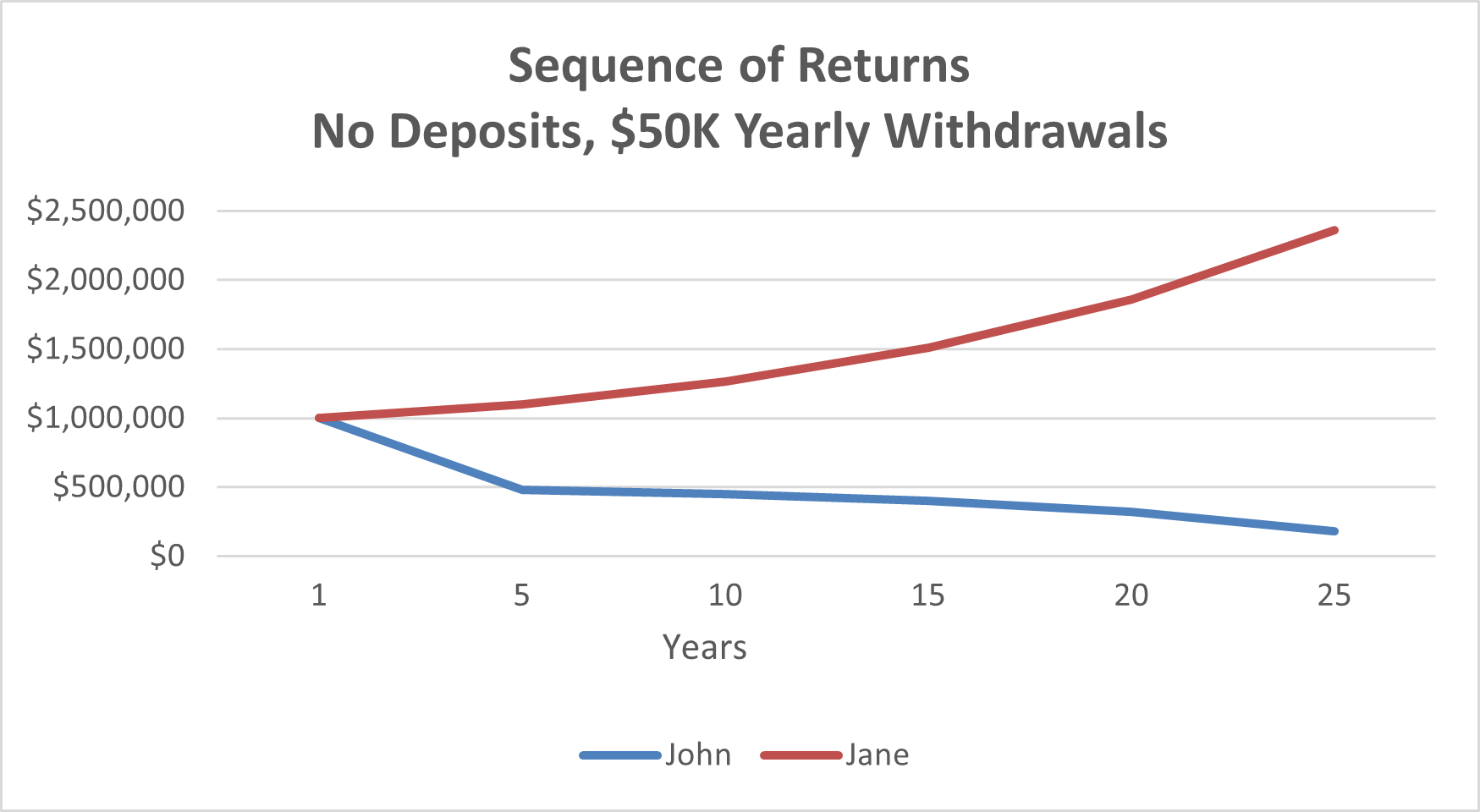

Consider two retirees, John and Jane:

- Both retire at age 65 with $1 million invested in stocks.

- Both withdraw $50,000 annually at the start of each year (not adjusted for inflation).

- Both earn an average annual return of 7.55% over 25 years.

The only difference is the timing of their returns.

- John experiences a –30% return in his first year and –20% in his second

- Jane earns steady positive returns early on

Even though both ultimately achieve the same average return, their outcomes diverge dramatically. John’s early losses combined with ongoing withdrawals significantly reduce his portfolio’s ability to recover. By the end of 25 years, he has only about $150,000 remaining.

Jane, on the other hand, benefits from positive early returns and ends up with approximately $2.5 million.

This hypothetical example is for illustrative purposes only and is not representative of any particular investment or portfolio nor do they reflect any investment fees, expenses, inflation or taxes. Other factors that may affect the longevity of assets include the investment mix, taxes, expenses related to investing and the number of years of retirement funding (life expectancy). Past performance is no guarantee of future results.

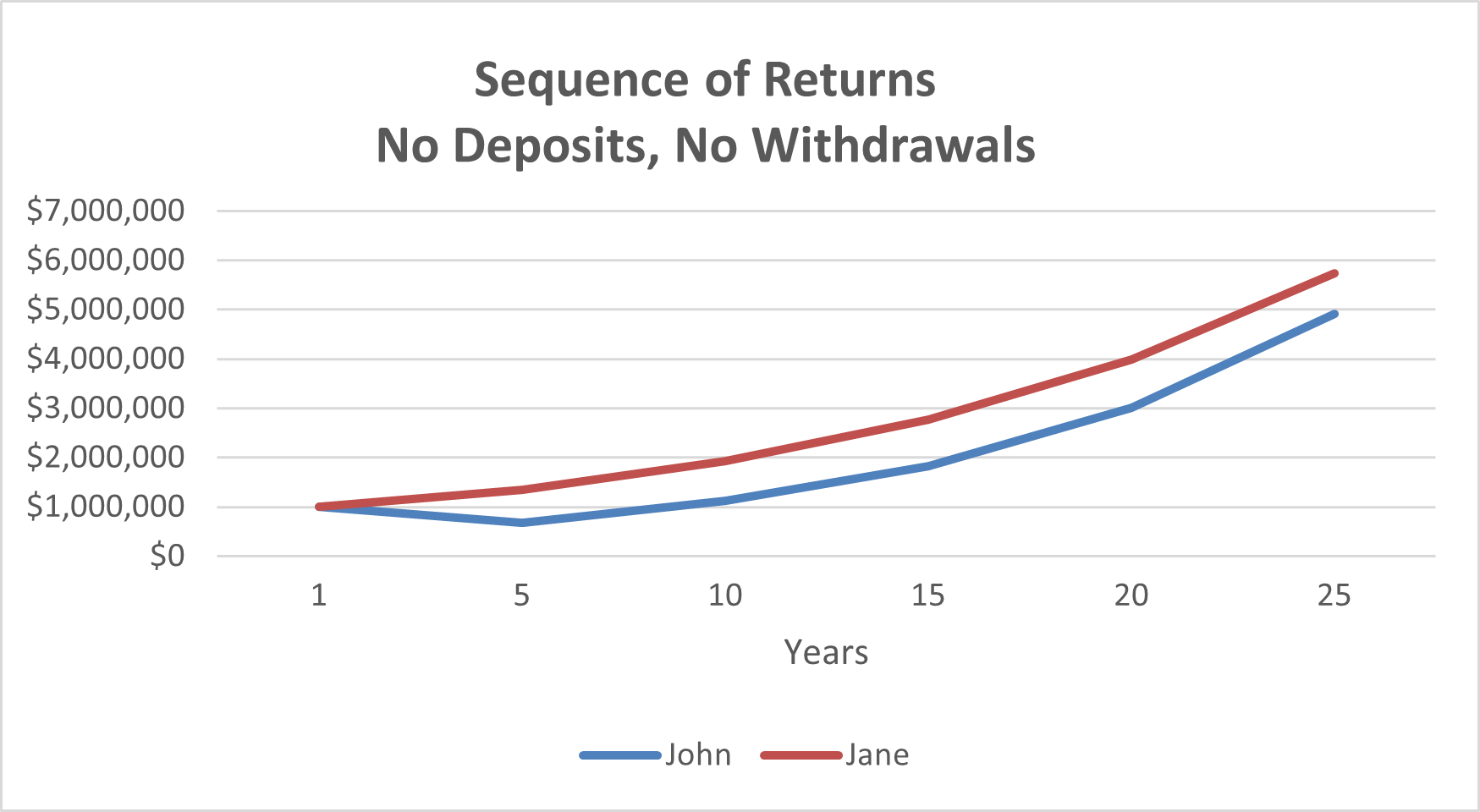

Interestingly, if neither had made withdrawals, their ending balances would have been much closer. This highlights a key point: sequence risk is most impactful during the withdrawal phase of retirement, not during accumulation.

This hypothetical example is for illustrative purposes only and is not representative of any particular investment or portfolio nor do they reflect any investment fees, expenses, inflation or taxes. Other factors that may affect the longevity of assets include the investment mix, taxes, expenses related to investing and the number of years of retirement funding (life expectancy). Past performance is no guarantee of future results.

Managing the “Wild Card”

As the last couple of years have clearly demonstrated, no one can reliably predict what the markets will do next. Market movements are inherently unpredictable. Downturns often arrive without warning, and some of the strongest recoveries occur during periods of uncertainty. Because of this, attempting to time the market or predict short-term movements is rarely effective.

A sound approach is to maintain a low-cost, globally diversified portfolio aligned with your goals and risk tolerance. Investment strategies should be driven by your personal circumstances not by market headlines or emotional reactions.

That said, while you can’t eliminate sequence risk, you can take steps to reduce its impact.

Practical Strategies to Mitigate Sequence Risk

1. Stay Flexible with Retirement Timing

If possible, delaying retirement or working part-time can reduce the need to draw from your portfolio during market downturns. Even modest income can help preserve your investments during vulnerable periods.

2. Adjust Spending When Needed

Reducing withdrawals especially in the early years of retirement can significantly improve your portfolio’s longevity. Temporary spending cuts during market declines can allow your investments time to recover.

3. Diversify Income Sources

Relying solely on equities for income can increase risk. Drawing from other sources such as cash reserves, bonds, Social Security, pensions, or annuities can help you avoid selling stocks at depressed prices. Some retirees divide their assets into short-, medium-, and long-term buckets. For example:

- Cash for near-term expenses

- Bonds for intermediate needs

- Stocks for long-term growth

This structure can provide stability and reduce the need to tap equities during downturns.

5. Consider Dynamic Withdrawal Strategies

Instead of withdrawing a fixed amount each year, some retirees adjust withdrawals based on market performance. Taking less after a down year can help preserve portfolio longevity.

6. Work with a Financial Advisor

Sequence risk is just one piece of a broader retirement strategy. Tax planning, withdrawal sequencing, investment allocation, and longevity considerations all play important roles. A thoughtful, coordinated plan can help you navigate these complexities more effectively.

Final Thoughts

Sequence risk highlights an important truth about retirement planning: it’s not just how much you earn, but when you earn it that matters.

While no one can control market timing, building a flexible, well-diversified plan and being willing to adjust along the way can go a long way toward protecting your financial future.

If you’re approaching retirement or already drawing from your portfolio, now is a good time to evaluate how sequence risk could affect your plan and what steps you can take to manage it effectively.