Social Security Break-Even

Financial Planning RetirementSince the passage of the Social Security Act in 1935, Americans have continued to ask the same important question: “When should I begin claiming Social Security benefits?” The answer remains as elusive as ever. Although break‑even analysis offers a helpful starting point, the best timing ultimately depends on your health, financial situation, and long‑term goals.

Let’s take a closer look at how to find the right balance for you.

For most people, full retirement age (FRA) falls between 66 and 67, depending on birth year. Benefits can begin as early as age 62 or be delayed until age 70. Claiming at 62 provides more years of payments, though at a reduced monthly amount. Delaying until 70 produces the highest monthly benefit but requires forgoing several years of payments.

Finding your break‑even age, the point when delaying leads to a higher lifetime total, can help frame your decision.

For example:

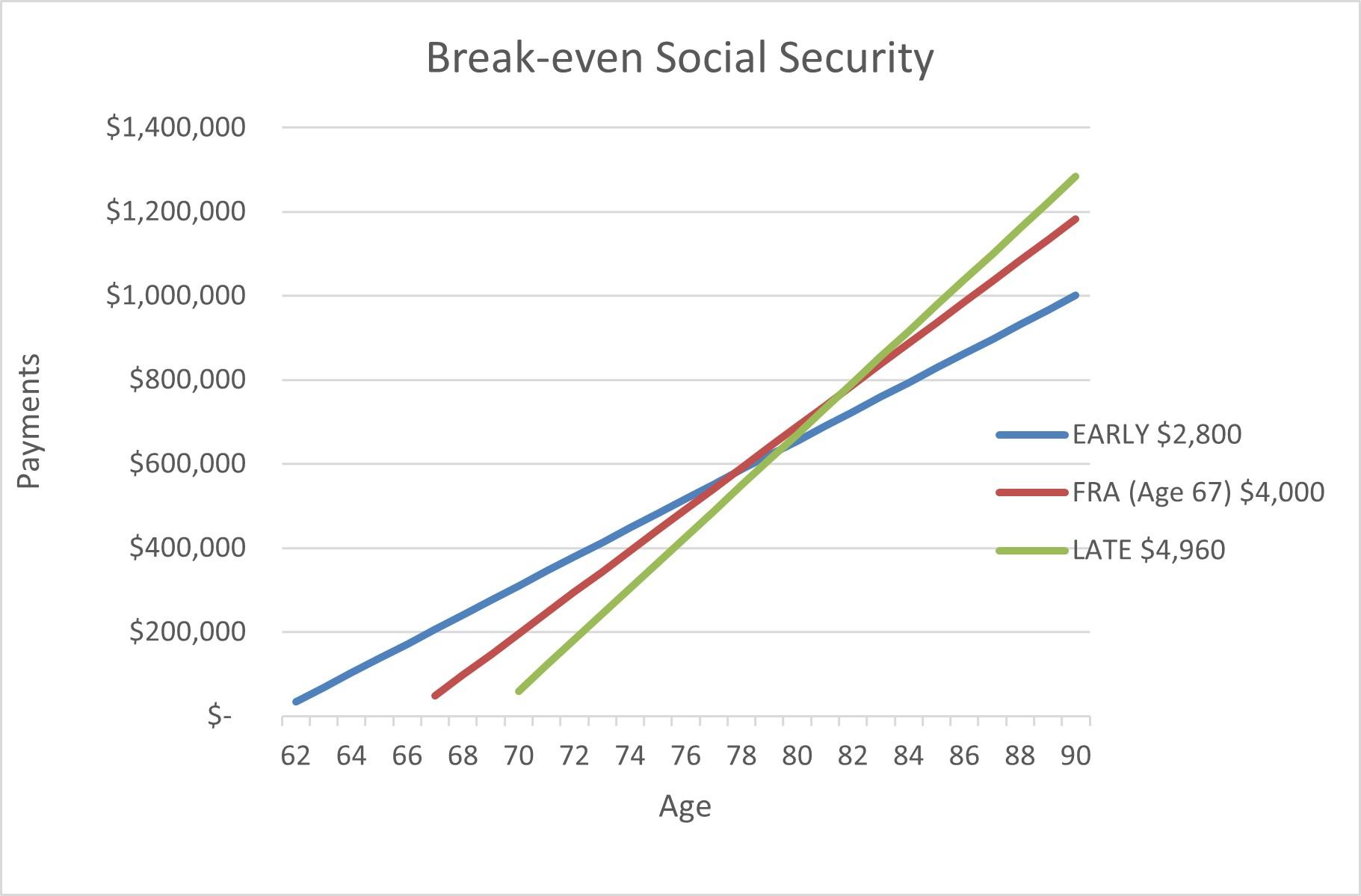

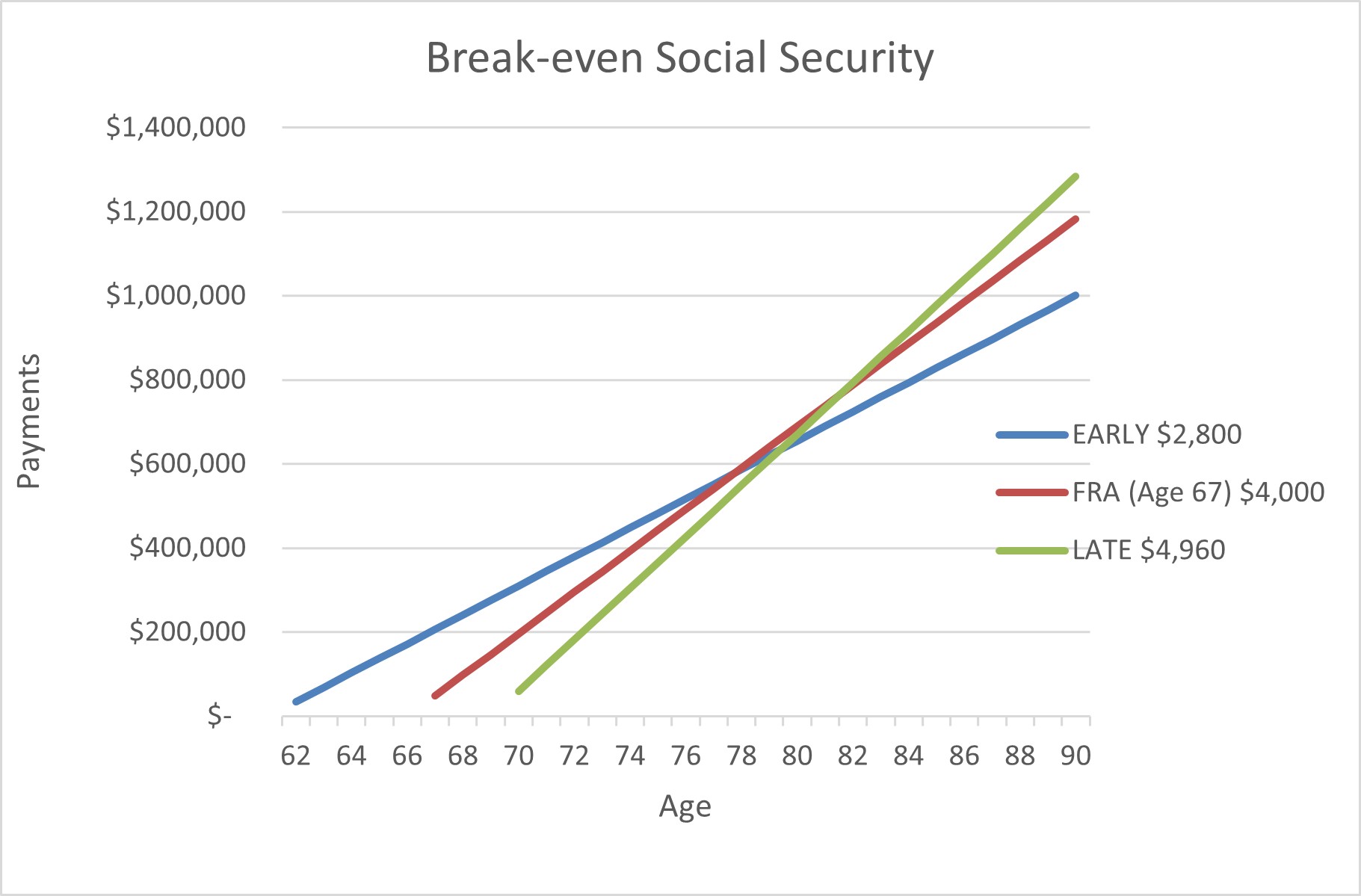

- Age 62 vs. 67: Break-even at ~78; delaying yields about a 30% higher monthly benefit.

- Age 67 vs. 70: Break-even at ~82; delaying adds roughly 24% to your monthly benefit.

- Age 62 vs. 70: Break-even at ~80; this is when the maximum benefit eventually overtakes early claiming.

Your expected longevity plays a critical role. While no one can predict life expectancy with certainty, health status and family history can provide useful context.

An Example

There are more than three options for when to start claiming Social Security benefits. In fact, you can choose any point after you reach your early retirement age of sixty-two (62). For every month between the ages of 62 and 70, your monthly benefits will increase. (You can wait longer than age seventy (70), but your benefits will not continue to grow.) Any two points between ages 62 and 70 will have their own break-even.

Let’s consider the three scenarios above: age 62 (early), age 67 (FRA), age 70 (late).

If you chart the accumulated benefits of those three scenarios on a line graph, you will find the break-evens where the lines intersect:

There is a lot of math to consider, including a key variable we have not discussed: how long you expect to live. Of course, none of us can predict our life expectancy with any certainty. But we can make some educated guesses based on factors like our current health and our family medical history. For instance, if both of your parents lived well into their 90s, you might have more confidence in your own life expectancy.

Other Important Considerations

Break-evens are a useful tool in deciding when to start claiming Social Security benefits, but they are not the only or most crucial factor. For example, you may prefer to have more money in the early part of your retirement so you can spend more on the experiences money can buy.

Following are some of the most common factors that may influence whether to start taking Social Security sooner or later.

- Alternate Income Sources: First, and most obviously, if you have few or no alternate income sources once your paychecks stop, you may not have the luxury of waiting until you are 70. You may need to start taking Social Security as soon as possible.

- Life Expectancy: Delaying benefits generally assumes you will live to, or beyond, the average age projected for your demographic. Personal health and lifestyle should guide how realistic this is.

- Estate Planning: Your priorities for leaving assets to heirs or charities may affect how you draw from savings and when you choose to claim Social Security.

- Employment: Working before reaching FRA may reduce benefits:

- Before FRA: $1 withheld for every $2 earned above $24,480.

- Year you reach FRA: $1 withheld for every $3 earned above $65,160 (earnings before your birthday month).

- At FRA and beyond: No earnings limit.

- Marital Status: Married couples face additional considerations, including different ages, life expectancies, and the availability of spousal, survivor, or ex‑spouse benefits. All these factors can complicate the equation. Ideal start dates for one scenario may not be ideal for another.

- Other Personal Circumstances: Factors such as business ownership, living abroad, disability eligibility, or dependents receiving benefits can also influence the optimal claiming strategy.

- Income Taxes: Up to 85% of Social Security benefits may be taxable, depending on your combined income. Social Security income also affects your modified adjusted gross income (MAGI), which determines potential Medicare premium surcharges beginning at age 65. Bottom line, broad tax planning could influence your timing.

We don’t expect you to calculate break-evens for every possible scenario. Understanding the concept of break-even will help you take a more informed approach to this major decision on your retirement journey.

We are here to help you and your family make good choices about when, and how to manage your available options and more importantly how they might fit in with your larger financial picture and retirement goals. As always, the best choice is the one that makes the most sense for you.