The Hidden Costs of Index Rebalancing: What Investors Should Know

InvestmentEvery June, one of the largest trading events in the U.S. stock market takes place with little public attention. As major indexes are rebalanced, hundreds of billions of dollars can be forced into the same trades at the same time. While this may seem like a technical market event, it highlights an important reality for investors: index changes can create temporary price distortions that may impact investment returns.

Each year, Russell reviews which companies belong in their large-cap and small-cap indexes. As businesses grow, shrink, merge, or go public, the indexes are updated to reflect the current market. The annual FTSE Russell index reconstitution is scheduled for the fourth Friday in June. This is the process Russell uses to update its U.S. indexes, so they better reflect the current market.1

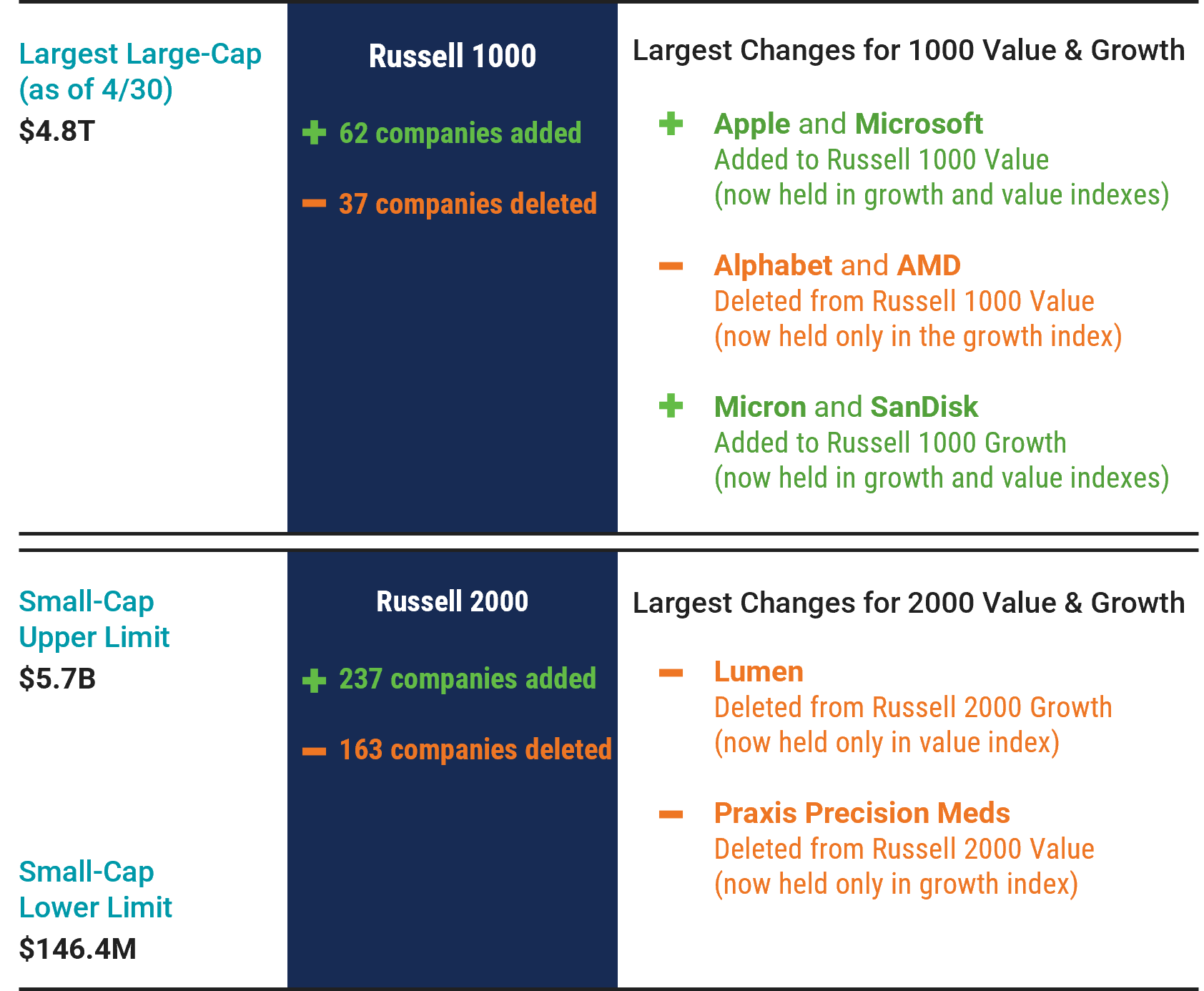

Figure 1 highlights some of the more notable changes expected this year.

Figure 1 | June 2026 Russell Index Reconstitution Highlights

Sources: Avantis Investors, FTSE Russell.

1. Russell announced that the June 2026 reconstitution will be the final annual rebalance of its U.S. equity indexes. Going forward, the indexes will be reconstituted semi-annually (June and December) starting in December 2026. Past performance is no guarantee of future results.

At first glance, this may sound like a routine index update. But it can matter because funds that track these indexes often need to make a large number of trades at the same time. That can create unnecessary tax and trading costs by forced trades: selling securities leaving each index; buying securities joining each index and adjusting the old weights of securities staying in each index to their new weights by buying and/or selling securities.

Because so much money tracks Russell’s U.S. indexes, these updates can lead to an unusually large amount of trading in a single day. For some securities, trading tied to the reconstitution can be many times higher than normal.

When hundreds of billions of dollars are directed into the same securities on the same day, prices can temporarily move away from fundamental value. Stocks being added to an index often experience buying pressure, while stocks being removed can face selling pressure.

A simple illustration:

Imagine a stock that is being added to a major index. Index funds tracking that benchmark must purchase shares regardless of valuation. If many funds are competing to buy the same stock simultaneously, the price may rise temporarily. Investors purchasing after the announcement may end up paying more than the company's fundamentals justify.

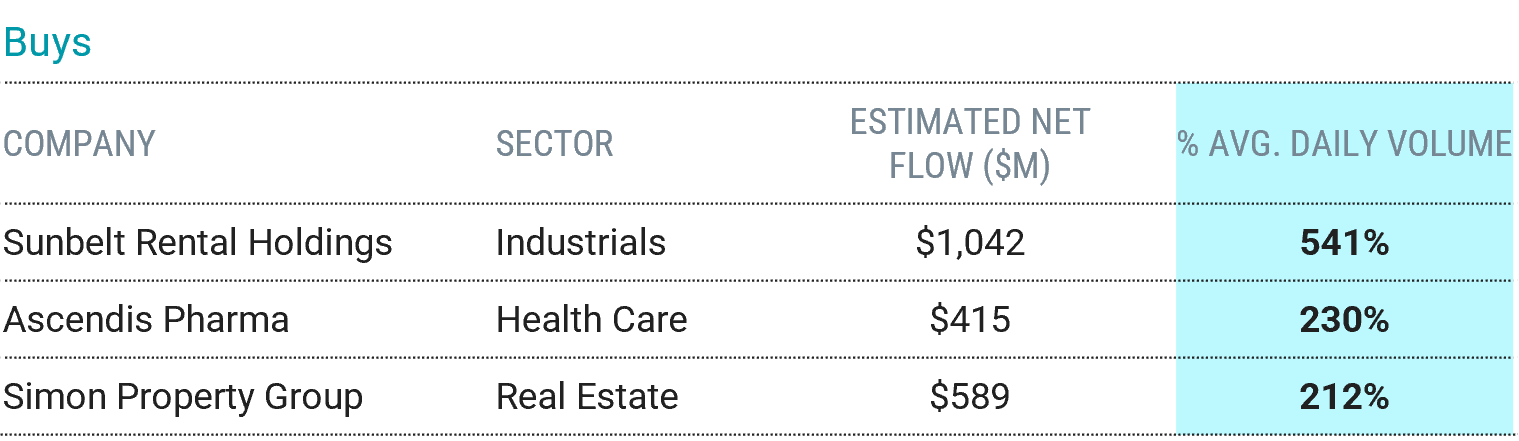

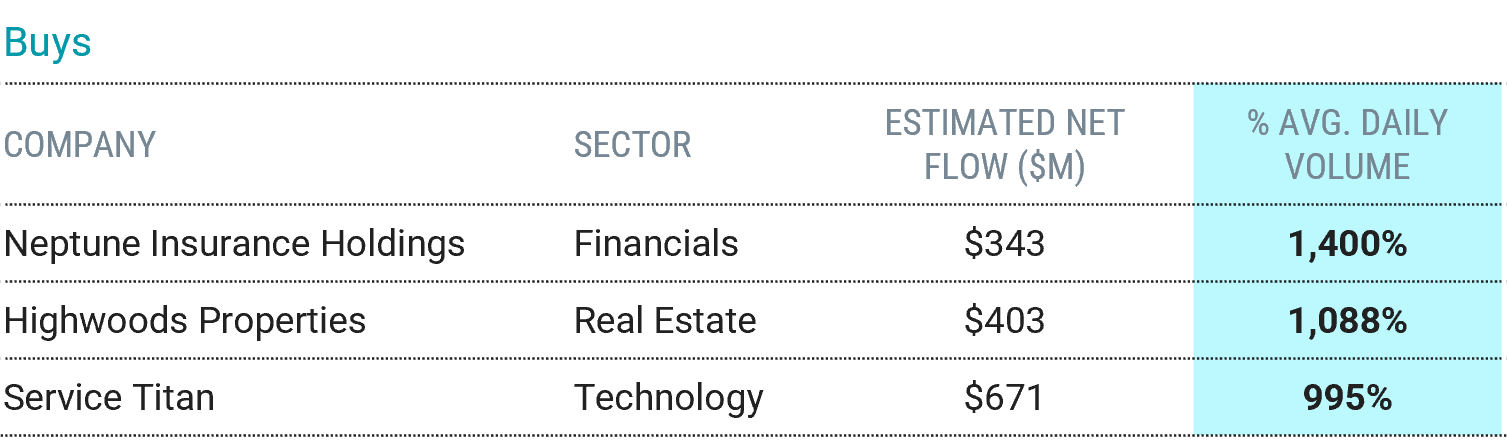

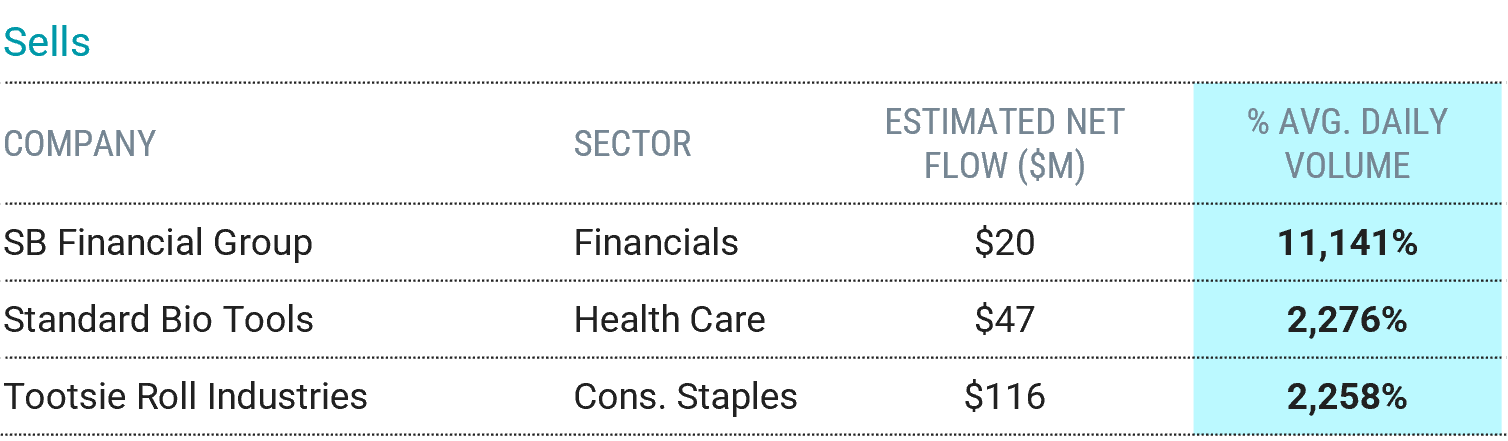

As shown in Figure 2, some of the stocks affected may need to trade at levels far above their usual daily volume.

Figure 2 | Too Much to Trade?

Highest Expected % of Average Daily Trading Volume among Largest Announced Buys and Sells during the June 2026 Reconstitution

Panel A | Russell 1000

Panel B | Russell 2000

Sources: Avantis Investors, Jefferies.

That raises an important question: Is concentrating so much trading into one day the best approach for investors? When many funds need to buy or sell the same stocks at once, prices can move in ways that make trading more expensive.

For example, if a fund must quickly buy a stock that is being added to an index, it may have to pay a higher price. If it must sell a stock leaving an index, it may have to accept a lower price. Those costs may be easy to miss, but they can still affect returns over time.

Researchers have studied these effects around index rebalances, and the results suggest the costs can be meaningful. While estimates vary, the broader takeaway is straightforward: when index changes lead to rushed trading, investors may end up paying more than they realize.

This is one reason we favor a flexible, evidence-based investment approach rather than relying solely on traditional index construction and waiting for a once- or twice-a-year index reset to drive trading. By evaluating securities continuously rather than waiting for periodic index changes, investors may avoid some of the unnecessary trading costs associated with large benchmark rebalances.

Disclaimer: This approach may be appropriate for some investors and is not a recommendation for all investors as investment approaches should be tailored to individual circumstances.

The June Russell reconstitution is a useful reminder that markets are not always perfectly efficient. Large institutional flows can influence prices in the short term, creating opportunities and risks that have little to do with a company's underlying fundamentals. For long-term investors, maintaining a disciplined process and focusing on fundamentals remains more important than reacting to benchmark-driven trading activity.